How Factoring Businesses Can Protect Against Fraud in 2026

It happens every day. A factoring business thought they were funding a reliable new client. The invoices checked out, and the business seemed legitimate until the debtor swore they’d never done business with that “client.” By then, hundreds of thousands of dollars were gone.

Stories like this aren’t rare. Fraudsters are getting smarter, and factoring businesses are often right in their crosshairs. As we head into 2026, the question isn’t if your factoring company will face fraud attempts; it’s when.

The good news? With the right strategies, you can protect your portfolio, your clients, and your reputation.

Let’s dive into the latest fraud trends and compliance requirements for factoring companies to ensure a secure and prosperous future.

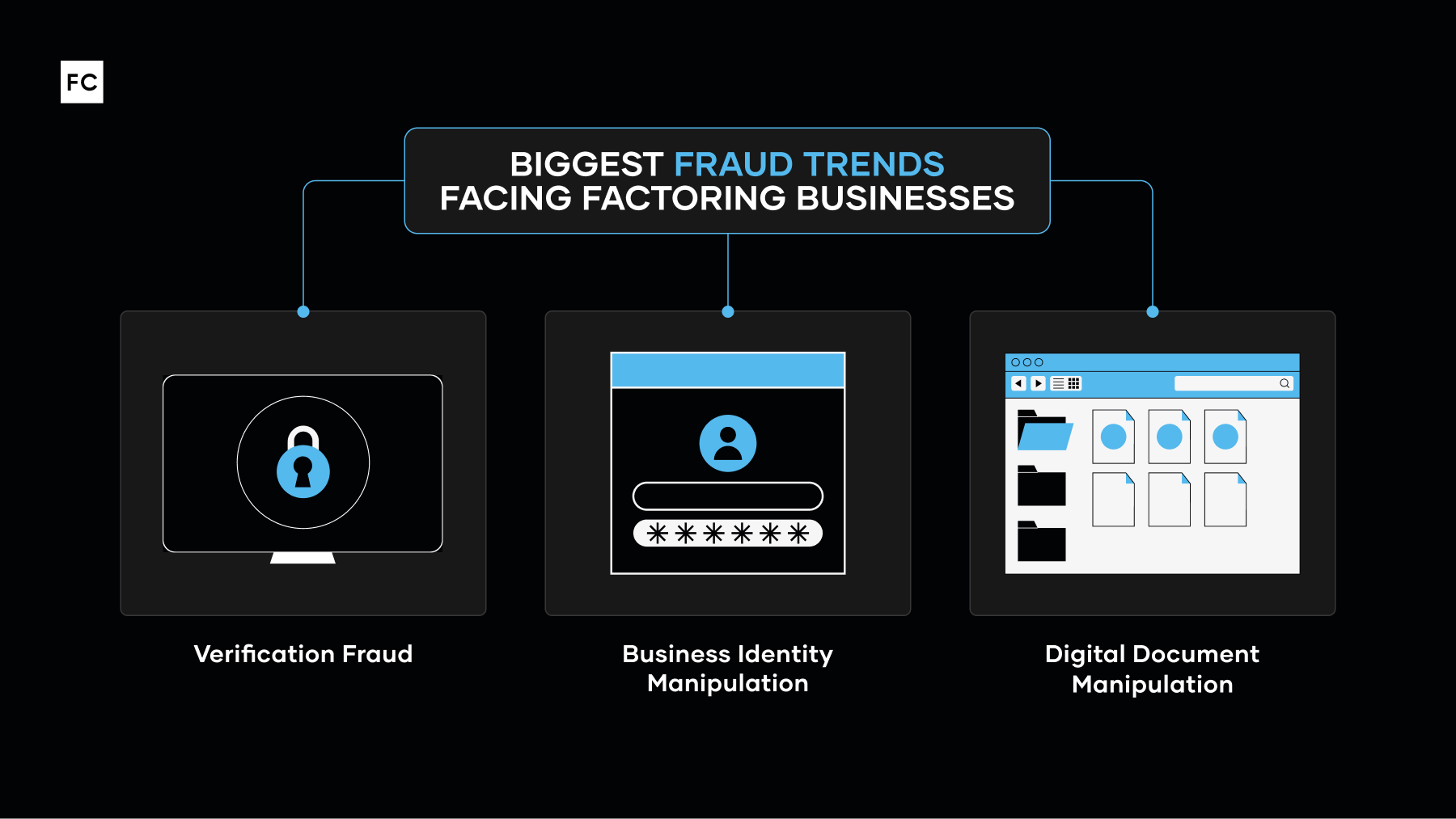

What Are the Biggest Fraud Trends Facing Factoring Businesses?

Fraudsters are constantly evolving their tactics, leveraging new technologies and exploiting vulnerabilities. For factoring businesses, staying ahead requires vigilance and adaptive strategies. Industries like the trucking industry are especially vulnerable to sophisticated fraud schemes due to their heavy reliance on factoring services.

1. Verification Fraud & Business Identity Manipulation

One of the most insidious threats is the manipulation of business identities to create fictitious entities or impersonate legitimate ones. This can involve:

- Impersonation: Fraudsters posing as employees or owners of a real business, submitting fraudulent invoices

- Synthetic Identities: Mixing real and fake information to create a new “business” identity that appears legitimate during initial checks

- Shell Companies: Creating non-existent businesses to generate fake invoices and receive advances

These schemes aim to secure factoring services for non-existent receivables, which can lead to significant losses for the factoring company.

2. Digital Document Manipulation

Fraudsters are also using advanced editing tools to falsify the documents that factoring businesses rely on. These can include:

- Invoices: Altered amounts, duplicated submissions, or entirely fabricated transactions

- Bank Statements: Modified balances or transaction histories to inflate financial health

- Proof of Delivery (PODs): Forged signatures or doctored shipping records to “validate” nonexistent loads

These fake documents are increasingly difficult to detect through manual review, making factoring companies more vulnerable to well-crafted fraud attempts.

Why Fraud Prevention Factoring Must Be a Priority

Effective fraud prevention factoring isn’t about avoiding losses; it’s about maintaining trust, protecting reputation, and ensuring operational stability. The cost of a single major fraud incident can be financially catastrophic for client relationships and market standing. Prioritizing fraud prevention strengthens the entire business model.

Core Principles for Fraud Detection in Financial Services Use

The principles of fraud detection in financial services apply universally, but they are particularly crucial for factoring companies. Here are the biggest things to keep in mind:

- Continuous improvement: As fraud tactics evolve, so must your prevention strategies. Regularly review and update your methods.

- Collaboration: Share insights and best practices within the industry (where appropriate and secure) to collectively strengthen defenses.

- Data-Driven Decisions: Leverage data analytics to inform your fraud prevention strategies, understanding where and how risks will likely materialize.

- Layered Defenses: No single solution is foolproof. Implement multiple layers of security, from strong onboarding processes to continuous monitoring.

Key Compliance Requirements for Factoring Companies

Adhering to compliance requirements for factoring companies is not merely a legal obligation but a large component of factoring risk management. Regulations like Anti-Money Laundering (AML) and Know Your Business (KYB) are designed to combat illicit financial activities, including many forms of fraud:

- KYB: Thoroughly vet all clients and their debtors; this includes verifying business registration, beneficial ownership, physical address, and financial health

- AML: Implement robust producers to detect and report suspicious transactions that could indicate money laundering activities

- Data Security and Privacy: Protect sensitive client data and financial information in compliance with data protection regulations

- Reporting Requirements: Understand and fulfill all regulatory reporting obligations related to suspicious activities

Organizations such as the Commercial Finance Association and the International Factoring Association offer best practices, training, and resources to help factoring companies stay compliant and up-to-date with industry standards.

How to Detect Fraudulent Invoices as a Factoring Business

Detecting fraudulent invoices is at the heart of factoring fraud prevention. Here are some key points on how to detect fraudulent invoices as a factoring business:

- Debtor Verification: Always verify invoices directly with the debtor to confirm their legitimacy and the services/goods rendered.

- Invoice Red Flags: Look for inconsistencies such as:

- Unusually high invoice amounts for a new client or specific debtor

- Invoice with vague descriptions of goods or services

- Invoice without standard company logos, contact information, or proper formatting

- Sequential invoice numbers that seem out of order or rapidly increase

- Duplicate Invoice Detection: Implement systems to identify if the same invoice (or a similar one) has been submitted multiple times or to various factoring companies.

- Behavioral Analysis: Monitor client and debtor behavior, especially sudden changes in payment patterns, invoice volume, or communication.

- Industry Benchmarking: Ensure invoice values and payment terms are plausible for the client’s industry.

- Document Forgery Checks: Utilize software to detect forged documents, such as altered purchase orders or shipping receipts.

Fraud Detection Using Machine Learning & AI

As fraudsters deploy sophisticated tools, factoring businesses can leverage their advanced arsenal. AI and Machine Learning (ML) are becoming indispensable tools in the fight against factoring fraud.

- Anomaly Detection: ML can flag unusual invoice amounts, frequencies, or debtor behavior that deviates from established norms, indicating potential fraudulent activity.

- Predictive Analytics: AI can analyze large datasets of transactional history, client behavior, and industry benchmarks to identify patterns indicative of fraud that human eyes might miss.

- Real-Time Monitoring: AI-powered systems can monitor transactions in real-time, allowing for immediate intervention when suspicious activities are detected, significantly reducing potential losses.

Factoring Risk Management: Building a Culture & Infrastructure for Accounts Receivable Financing

Effective factoring risk management goes beyond a checklist; it requires a holistic approach that permeates the entire organization.

- Culture of Vigilance: Build an environment where every employee understands their role in fraud prevention and feels empowered to report suspicious activity.

- Robust Technology Stack: Invest in advanced fraud detection software, secure data management systems, and identity verification tools.

- Regular Training: Provide ongoing training to staff on the latest fraud trends, internal policies, and how to use prevention tools effectively.

- Clear Policies and Procedures: Documents clear, actionable policies for client onboarding, invoice verification, and suspicious activity reporting.

- Dedicated Risk Team: Establish a dedicated risk management team responsible for monitoring, analyzing, and responding to threats.

Employee Education & Training: Empowering Your Team Against Fraud

Your team is your first line of defense against fraud in today’s factoring landscape. By giving your staff a deep understanding of accounts receivable, cash flow management, and invoice factoring, you equip them to spot red flags and make smarter decisions.

Training should cover the essentials of invoice factoring, current trends in global factoring services, and the unique risks tied to receivable financing. Regular workshops and ongoing learning keep your team ahead of evolving fraud tactics, from fake invoices to unusual payment requests. Beyond detection, this approach fosters a culture of transparency and accountability, which is a competitive advantage.

Business Continuity Planning: Ensuring Resilience Amidst Fraud Threats

Companies that rely on factoring services for cash flow need robust plans to protect operations from cyber threats and unexpected disruptions.

Effective continuity planning starts with identifying potential risks and creating strategies to mitigate them. This includes rapid-response protocols, secure data backups, and reliable support from your factoring provider. Partnering with experienced providers, such as FactorCloud, can further strengthen your resilience with tailored financial solutions and expertise in asset-based lending and purchase order financing.

Emerging Threats to Watch in 2026

As the landscape of factoring fraud continually shifts, generative AI is the most significant emerging threat to watch in 2026. Fraudsters now use sophisticated AI models to create persuasive fake documents, forged emails, and even realistic voice impersonations. This technology makes traditional verification methods less reliable and poses a serious challenge to standard due diligence, which means factoring businesses need to adopt more advanced detection strategies.

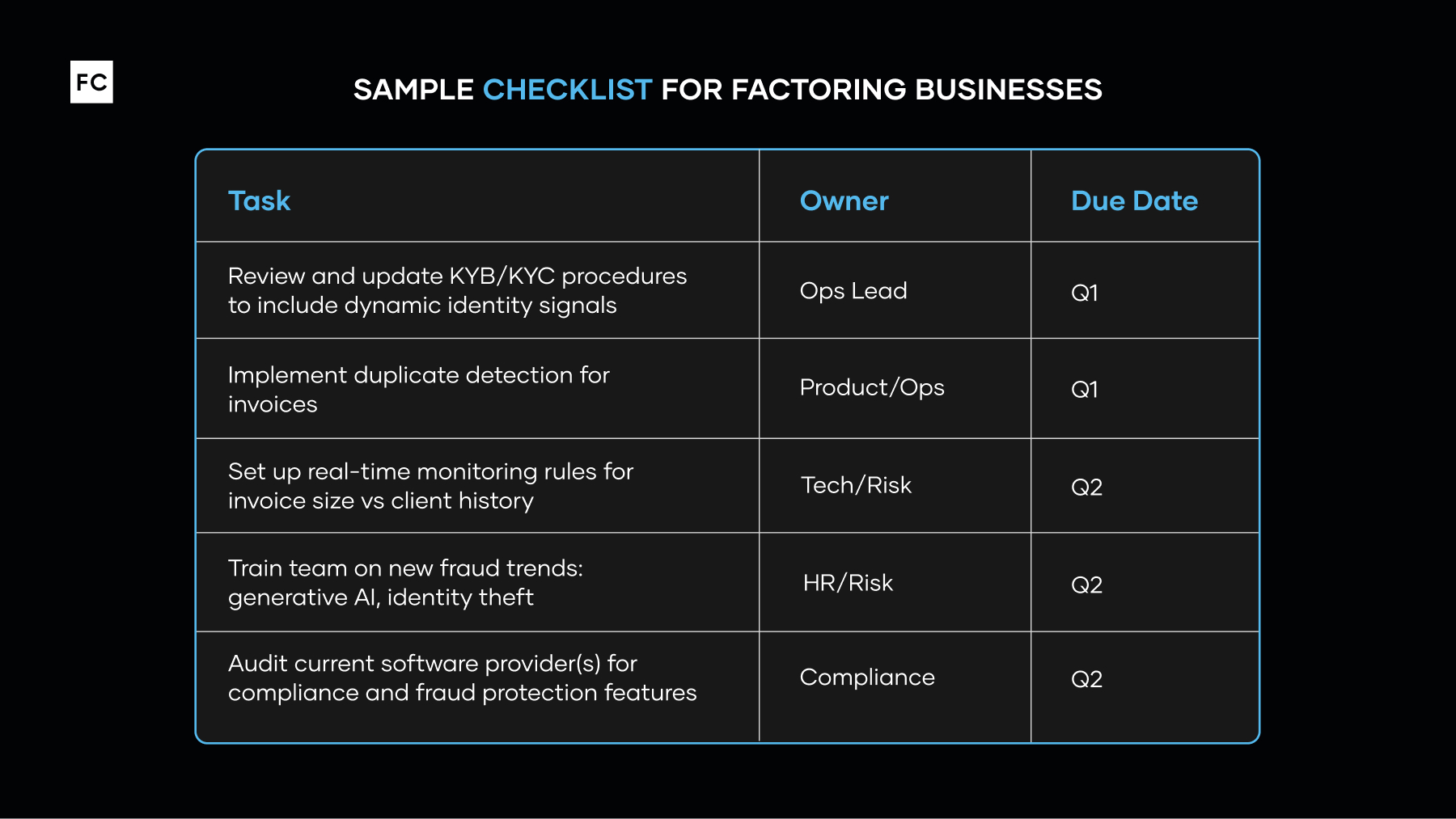

Action Plan: What Factoring Businesses Should Do Now

Here’s an example checklist you can use this quarter to strengthen your fraud prevention factoring approach:

Why Compliance Requirements for Factoring Companies Go Hand-in-Hand with Growth

Many factoring businesses view compliance as a necessary but complicated cost of doing business. However, the most successful firms understand that strong factoring company compliance is not a barrier to growth—it’s a catalyst for it.

A strong compliance framework, built on rigorous KYB/KYC and AML procedures, acts as a powerful filter, weeding out high-risk or fraudulent clients before they can cause financial or reputational damage. This builds a foundation of trust that attracts larger, more reliable clients and unlocks access to better funding sources. When investors and banks see a rock-solid compliance program, they see a well-managed, low-risk business worthy of their capital. In this way, treating compliance as a strategic asset rather than an obligation directly fuels sustainable and profitable growth.

Strengthening Your Defenses for the Year Ahead

The fight against factoring fraud is not a one-time project; it’s an ongoing commitment. Your defenses must evolve to stay ahead of fraudsters.

The strategies discussed here are designed to build a resilient factoring risk management culture that protects your assets and reputation. By prioritizing proactive fraud prevention, fostering a vigilant team culture, and investing in modern technology, you're not just preventing losses—you're building a more secure and trustworthy business.

Turn to a Factoring Software Company You Can Trust

Ready to upgrade your factoring business with a modern, all-in-one software solution?

FactorCloud is designed to streamline your operations, minimize risk, and give you a competitive edge with features like:

- Automated Workflows

- Integrated Freight Verification

- Advanced Risk Management

- Powerful Reporting

Schedule a FactorCloud demo today and see how our intuitive platform can transform your factoring business.